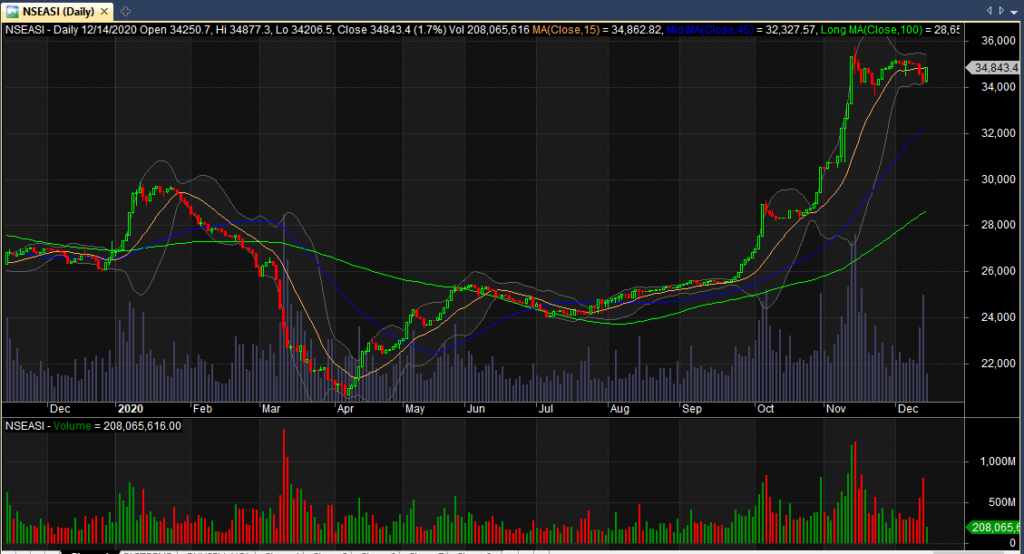

The Nigerian stock market ended the past week cumulatively on a bearish note.

The NSE All-Share Index and Market Capitalization depreciated by 0.63% and 0.61% to close the week at 40,186.70 index points and N21.026 trillion respectively.

Local investors are currently hunting for greater returns on investment thus increasingly selling off their equity positions and plowing the proceeds in fixed income instruments at a time majority of companies’ earnings reports for 2020 are yet to be issued.

“The unprecedented and highly stimulatory policy is an attempt to exceed one million jobs a month from April to September.“

The latest outcome of the Nigerian Treasury Bill auction points towards yield elevation in the short term.

The most recent data retrieved from CardinalStone Research revealed benchmark yields advanced by an average of 10 basis points.

The overnight and open buyback rates rose by c.17.00% apiece to 20.50% and 20.00% respectively, following the retail FX auction conducted last Friday alongside OMO and bond auction settlements.

Also, the sentiment seems to have reversed given the mixed signal from the fixed income market that yields may begin to rise faster-than-anticipated after the outcome of the last OMO and NTB auctions conducted by the CBN,” said Abiodun Keripe, Managing Director, Afrinvest Research.

On the foreign side, Stephen Innes, Chief Global Market Strategist at Axi spoke on the same prevailing conditions weighing hard on the world’s biggest and most liquid stock market. He buttressed more on rising U.S Treasury yields, an arch-enemy to U.S stocks, as investors switch their attention momentarily to the bond market;

“US equities were weaker Friday while US 10-year yields rose a further 4bps to 1.34%. Those moves were capping off the overriding trend in markets last week: growing concerns about inflation risks pushing nominal bond yields higher and weighing on the equity rally.

“The Biden administration continues to stay on message stressing Congress’s need to pass a significant fiscal package downplaying recent more robust economic data as its full-throttle as a package exceeding US$1.9 trillion heads for a House vote this week in a fast and furious attempt to get the US back to full employment next year.

“The unprecedented and highly stimulatory policy is an attempt to exceed one million jobs a month from April to September. Still, it underscores the narrower timeline from easing to tightening than post-GFC. And suggest taper tantrum fears are understandable even if severe inflation is still a 2022 issue,” Innes said.

What to expect: That being said, timing is still everything. The next leg of the reflation will have to be carried more and more by a continued recovery in economic growth, as fiscal and monetary stimulus gets increasingly packed into the prices of global equities.

You must be logged in to post a comment Login