MTN is a telecoms operator offering voice, data, and other enterprise mobility offerings. The telco, with over 21,900 employees, was founded in South Africa in 1994. As of March 2021, MTN had 280 million subscribers in twenty-one markets, including Nigeria.

The telecoms giant has announced a public offer of 575 million shares, offering the Nigerian market the opportunity to buy shares and become part owners of MTN Nigeria Plc. Using the current market price of MTN Nigeria at about N175, then potentially, the public offer should bring in about N100 billion if fully subscribed.

MTN is in the process of a strategic remake tagged the “Ambition 2025” that will see it focus squarely on Africa. The company wants to be the leading digital solution provider to drive African progress by 2025. This strategy will see the telco pivot from a “product” to a “platform” player. The company is expanding from traditional voice and data to digital via its ayoba® brand and FinTech via its MoMo® brand. Figure 1 details MTN growth platforms.

Why is MTN selling? Are they divesting from Nigeria?

The answer is no! MTN is not diversifying away from Nigeria. The telco’s public offer is in line with its Asset Realization and Portfolio transformation Program (ARP). MTN plans to sell down its shareholding in MTN Nigeria from the current 76% to 62%. It has concluded a similar “localization” in Zambia, selling 8% to the local market. The company intends to sell 12.5% of its holding in MTN Ghana and offer its shares in MTN Rwanda. They have sold holdings in their cell tower business in Ghana and Rwanda. They are also exiting their HIS Tower holdings which own cell tower assets in Nigeria. MTN has also diverted from Jumia Technologies AG, netting R2.3b ($138 million). In terms of divestment, however, MTN is exiting the Middle East entirely and has put up its 75% stake for sale.

Nigerian market key to MTN

Nigeria is MTN’s most profitable market, generating 32% (R57.9 million) of revenues; MTN South Africa generates about 25% (45.4 million) of revenues. Nigeria’s revenues for 2020 were up 14.6%. The MTN Group also allocated 38% (12.64) of all CAPEX expenditure in FY 2020 to its Nigerian operations. Nigeria generates a humongous amount of cash for MTN Group, with cash generated at about 37% (R17.23 billion) but took on 37% (R17.23 billion) of all reported Group debt.

ARP & debt reduction

MTN has two big problems; one is its huge debt overhang, the other is its Nigerian regulatory problem. Both issues are connected, and both can be solved by the company selling equity to the Nigerian market. The ARP objective is to reduce debt, simplify the portfolio, reduce risk, and improve returns. MTN plans to raise at least R25 billion over 3 to 5 years. A key revenue driver for the telco is debt reduction.

As of Q2 2021, MTN held SA 90.8 billion ($6.03 billion) in debt. For context, the telco’s short-term assets of SA 115 billion can cover its short-term liabilities of SA 108 billion. MTN, however, cannot cover its liabilities which will fall dues after 12 months with its short-term assets. MTNs Debt to Equity ratio at 83%, from 49% in Q3 2015, is high. Usually, debt to equity of 40% is appropriate. MTN, however, has sufficient cash cover from operations with a 74% Debt to Operations to Cashflow number. Also significant, MTN can service her interest payment with earnings generated up to four times Earnings before Interest and Taxes (EBIT). The risk for MTN is in its conversion of earnings to cash. Currently, MTN’s free cash flow is about 44% of its EBIT.

Again, even with this debt overhang, MTNs earnings using the Q2 report are about 19.7% a year; this is a faster growth rate than the SA market put at 11.3%. The telco’s historical annual earnings rate is at 35% and has beaten the SA industry and market, which return 21% and -5%, respectively.

Cashflow out of Nigeria, uncertain

The Nigerian government fined MTN Nigeria a record $1.5 billion for failing to disconnect its unregistered subscribers. MTN already paid a separate $53 million fine to the Nigeria Government after being accused of illegally repatriating about $8.13 billion to South Africa by the Central Bank of Nigeria (CBN). That is cash flowing out of MTN. The telco makes a lot of money in Nigeria but has seen its margins come under pressure and decrease to 50.9% from the effects of higher VAT and depreciation of the Naira, leading to the 29% increase in operating expenses. Simply put, revenues grew, but so did the costs of generating those revenues. Then the fines sucked out cash!

MTN has also struggled to get its cash dividends out of Nigeria and back to South Africa. The telco reported that it had repatriated $280 million in FY 2020 dividends from Nigeria in Q2 2021 report. This cash crunch was partly caused by slower repatriation of dividends from Nigeria. The payment of massive fines has created uncertainty, dented free cash flow, and seen MTN suspend dividends for FY 2020.

By selling equity, MTN Nigeria can raise cash from the Nigerian market, pay down debt and make a cash dividend payment to its investors.

Should I buy MTN Nigeria shares?

Invest according to your risk profile and objectives, but it is valid to note that MTN projected that its Nigerian unit would achieve double-digit growth in 2020; they were right as Nigeria’s growth was at 14.6%.

MTN Nigeria, to me, looks attractive on two levels

1. MTN is refocusing on Africa and is making Nigeria its vital market.

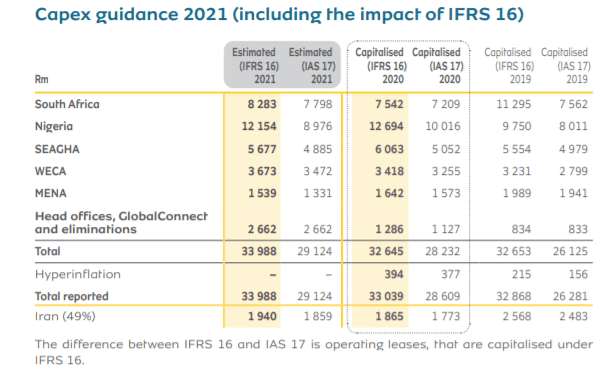

This is reflected in the massive CAPEX investment in the Nigerian franchise. These investments will strengthen the position of MTN in Nigeria. MTN has been listed as a 2021 priority to “accelerate Nigeria’s growth.” Figure 2 shows CAPEX investment in MTN Nigeria Plc.

Figure 2: MTN Nigeria CAPEX

2. Nigeria’s FINTECH opportunity

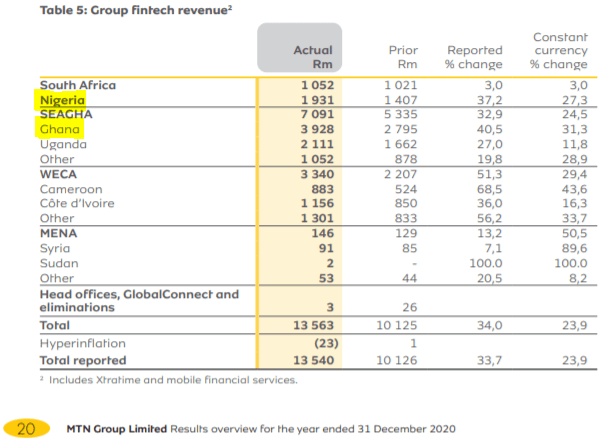

MTN makes its revenues from outgoing calls, data, and fintech, in that order. Revenues from FINTECH services in Nigeria were up 27%, with subscribers increasing eight times to 4.7 million supported by an agent network of 280,000.

While impressive, Nigeria’s FINTECH growth was constrained by the CBN not issuing MTN a mobile banking license similar to MTN Ghana MoMo®. MTN Ghana revenues from FINTECH in FY 2020 were R3.3 billion, while Nigeria reported just R1.58 billion from FINTECH revenues (see Figure 3). However, when you compare gross revenues generated from voice and data from MTN Nigeria and Ghana, Nigeria revenues far outpace Ghana. With the Approval in Principle of a payment service license by CBN to MTN Nigeria, the FINTECH offering will be more widely available to subscribers in Nigeria and help unlock growth and revenues. The telco could be the most significant FINTECH player in Nigeria and Africa. MTN stock is a proxy for the future of FINTECH in Nigeria.

See Figure 3: FINTECH revenues

There are many ways to participate in this offer, either via an application of MTN shares from your bank or stockbroker. You can also buy MTN via proxy by buying the Global X MSCI Nigeria ETF; this ETF holds about 4.80% of MTN shares.

Remember this is educational and not an offer to buy or sell, do your due diligence.

Article Originally Published Here